How blockchain, backlash, and breaches may challenge conventional wisdom and reshape your industry

The Official Future Hits Some Speed Bumps

Ask anyone in any major sector of the economy about the future of their industry and the majority will say something like the following:

- Our industry will be transformed by platforms

- These platforms will extract the most value from our industry and determine the winners and losers

- The most likely platform overlords will be the native digital tech giants: Google, Amazon, Facebook, Apple (or Alibaba and Tencent depending on where you live)

Essentially, what people are saying is that the notion of digital platform dominance is inevitable. In an Accenture survey in 2016, 81 percent of executives said platform based business will be core to their growth strategy within three years. As such, to understand where platforms are going is to understand the future of your industry itself. Either you will be that player (hard for most) or need to find a place to play and win within their ecosystem.

However, there are a few forces of change that are starting to erode this certainty and may lead to some surprising alternatives.

One of the game changers touted prominently in the past couple of years by technologists is blockchain. For many enthusiasts, blockchain technology promises to decentralize the digital realm and in doing so, re-democratize the economy as a whole. (See Stephen Johnson’s piece in the New York Times for a great summary of this idea.)

Meanwhile, what used to be quiet concerns expressed from legal and academic circles about “surveillance capitalism,” “black box society,” and similar concepts about handing over our daily decision making to the algorithms of companies like Facebook and Google — and business interests behind them — have now entered mainstream debate. The recent Cambridge Analytica/Facebook controversy is simply the latest wake up call to consumers about the risks of leaving perennial data trails in the hands of corporations. Already in Europe, the General Data Protection Regulation (GDPR) passed by the EU shows increasing political action that demands more transparency and self-directed control of where and how personal data is used.

Finally, people are starting to question whether the decisions being made on their behalf by these platforms are really in their best interest, or in the interest of the greater community. The fake news quandary has prompted calls to literally “delete Facebook”. In D.C., members of Congress (and the President) are directly expressing antimonopoly sentiments aimed at Amazon, similar to what the EU has been actively pursuing with Google.

Where Might Platforms Head? Multiple Scenarios Are In Play

As a result of these forces, we can plausibly ask whether the dominance of leading global platforms, in their current form, is at a peak. Over the next five to ten years (or maybe sooner), each of the forces above has the potential to either break apart the tightly integrated value proposition of leading platforms, or simply commoditize the core data ownership advantage upon which much of their success is built.

Using the principles of scenario thinking — that the future has multiple plausible, challenging and divergent possibilities — we can map out a few different potential ways in which this could play out. Depending on which set of early signs of change above become the dominant trend, we may end up with two or three alternative models for how digital and data-centric infrastructure might look, and therefore, a few different ways in which industries will organize in response. On the other hand, if none of these trends gains enough momentum, we could also continue on the current trajectory for a little while longer.

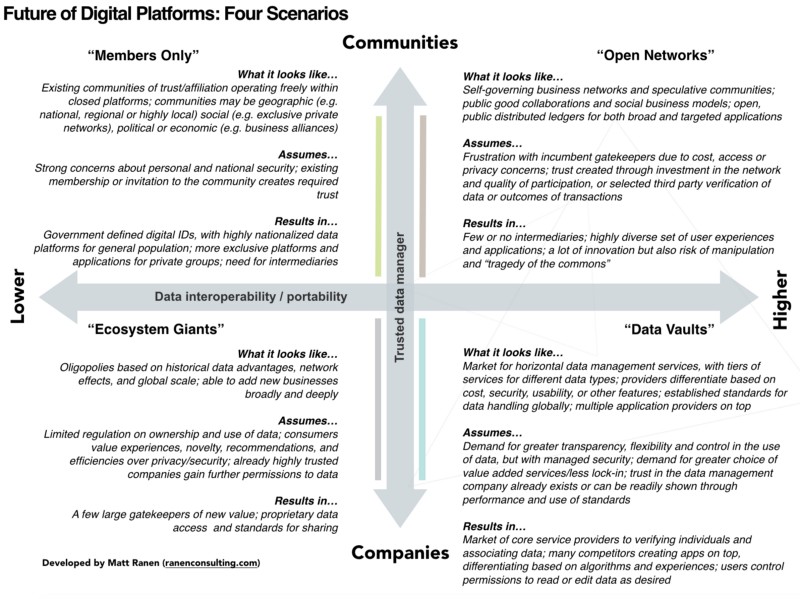

The diagram below frames up what I believe are the high level directions platform economies may head. At the core are two central questions:

1. What kind of control and access to data sets will be desired by consumers, and as importantly, demanded by regulators or other governance bodies? In the most narrow sense, will data interoperability and/or portability be higher or lower in the future?

2. Who will people trust to manage their data, starting with identities and core user profiles, but even moving to broader transactional and reputational histories? Will this continue to be the companies who are de facto doing this today — and according to polls, serving most of us pretty well? Or will it shift to communities, be they existing groups within which we have built up pre-existing relationships, or new purpose-specific networks?

While technology innovations are key enablers in many of these scenarios, they are not necessarily the primary drivers of mainstream adoption. These other important questions must be resolved for there to be a well defined and broadly accepted infrastructure.

The Official Future: “Ecosystem Giants”

The bottom left represents the current trajectory from today. It assumes a continuing, possibly even accelerating, land grab by the largest platforms into all types of industries and at all levels of participation. As with today, some of these ecosystems will be more open to partnerships than others, depending on who they are targeting. But all of them will build their advantage by leveraging more and more consumer and supplier data to do more and more things for those consumers and suppliers, which in turn will create a virtuous cycle that others could never re-create.

For example, in this future, Amazon takes over everything from shipping to healthcare; Facebook, Google and Apple finish splitting up the media sector and then backwards integrate into consumer products; and all of them do something in mobility. Just fill in your favorite platform and sector to play along.

In the end, this is a world of oligopoly. Consumers will need to choose to live in a particular ecosystem and likely, over time, be nudged towards the platforms’ preferences masquerading as their own. Although we will still see some spaces for innovation and competition, much of the value will return to the powerful platform owners.

Alternative Futures

The other three scenarios are different ways in which consumers, suppliers/producers and governments might respond to security concerns, fears of manipulation, or lack of choice.

Upper Left: “Members Only”

The upper left scenario, Members Only, is a world of heightened fear of external threats. Russian or North Korean hacking, Chinese spying, or even too much phishing from Nigeria, all lead to calls for improving the national digital security of the U.S. In this case, the common tendency will be to revert to interacting primarily within the communities people already know and trust. These are geographical communities — nations, states, cities, neighborhoods — or social or political affiliations. To get into each platform and enjoy its benefits you must be accepted more generally as member of the group. This includes companies too (with the recent Broadcom/Qualcomm decision providing another early sign of how security concerns may outweigh objectively sound business logic).

In this scenario, one can imagine government-issued digital IDs underpinning mainstream social media, commerce, legal, and even mobility, applications. It may be that the government itself will continue to add more data collection activities (for instance, China’s social credit system), build its own value-added applications, or outsource this to highly regulated companies. Or, in some countries, like the U.S., the natural limit of trust in government ownership may simply lead to less creative use of data overall.

In either case, to plug the gap of innovation, we will probably see more expensive, customized platforms and applications built for exclusive socioeconomic groups and purposes, where trust comes from rigorous vetting upon joining.

Overall, every platform and access to an industry ecosystem will work more like Next Door — where you need to verify that you live in a particular address and are an actual member of the neighborhood — but with even greater security protocols.

In the end, the convenience of today’s global platforms to move across goods and services without re-credentializing and with a high degrees of personalization will be traded in for security. Moving between different sectors and regions will require intermediaries and the overall resistance to let data move between countries — a form of data nationalism — will make it harder for a few dominant platforms to scale. Instead, they will have to go deeper into differentiating along a vertical line of business.

Making it Real: Consumer Finance in this Scenario

For example, in the payments industry, one can imagine a government digital ID system forming the backbone authentication platform for a host of services including a broadly accessible payments system for the mainstream. Meanwhile, on the high end, we might see exclusive, private systems — including private currencies or tokens — for what the industry calls “closed-loop marketplaces.” Both of these could nudge out Visa and Mastercard as the standard setters for authentication, and cut into the roles that banks and processors in their networks play. Instead, they would need to shift to more value added services in a more competitive part of the industry. India’s National Unique Digital Identity system (known as Aadhaar) and the associated payment system built around it are an early sign of this scenario.

Bottom Right: “Data Vaults”

Data Vaults is a world in which the backlash to the current platform regime is less about national security and more about the demand for greater transparency, flexibility and control in the use of data. It’s a world where consumers begin to complain about a lack of choice and want more options, but still want someone to manage their security. In this future, governments enact clear regulations about data ownership belonging to consumers themselves and standards for how data must be viewable and accessible. But the actual implementation, including standards for security, is left to the market.

In this scenario, one can imagine that consumer data management of all types becomes its own separate industry. Rather than letting the current platforms own their information in a proprietary way, consumers — or the apps they approve of — deposit information into large competing data vaults. These new, lower level platforms compete on price, differentiated security and other features, such as ease of use. And in a world that is interoperable, there are global standards for data handling and exchange, allowing for some degree of scale.

However, these base platforms will not have any advantage in providing value-added applications because consumers can choose to provide access to their data to anyone. Applications that are approved by the consumer can use this data or modify it if appropriate.

An analogy today is credit bureaus, but with much greater oversight and some additional room for differentiation. On top of the core data platforms, there will be intense competition to create compelling consumer apps, differentiating based on algorithms — i.e. how good they are in exploiting the data — and the quality of the experiences they provide.

Over time, the biggest risk will still be governance of these corporate entities and perhaps, similar oligopolistic behavior that would diminish quality and raise costs. And to a further extreme, this may result in a few different “data operating systems” to which apps will need to port, which will increase costs and limit choice too.

Making it Real: The Media Industry in this Scenario

In this scenario, in the media industry, we might see the advantages of Netflix and YouTube — and their powerful recommendation engines and product development research analytics — diminish. Instead, the open access to data might shift advantage to a combination of targeted analysis companies, who who can best interpret what viewers want to see from a widely available set of perennial and collective watching histories, and content producers, who can execute these with the most creativity. The aggregators wouldn’t aggregate proprietary content anymore. Instead, they would simply aggregate data.

Upper Right: “Open Networks”

The Upper Right is a world in which there is both a mainstream fear of too much government surveillance and a sense of unfairness about paying high fees to a large corporate entity just to hold what is yours (the equivalent of railing against bank fees). In this scenario, we move towards the more libertarian and/or democratized capitalism vision that blockchain promises. This is a world of self-governing business networks and high risk speculative communities. It’s also a world of non-profits or cooperatives collaborating on public goods or social business models.

In this scenario, one can imagine core data platforms powered by fairly open blockchain networks, where a minimum level of participation creates the initial trust to transact, and there are few, if any large intermediaries extracting rent. We will likely see a lot of innovation, both in terms of the core governance models themselves, as well as a wide range of applications and experiences built on top.

However, as we have seen with Bitcoin exchanges, there is also a risk of manipulation. And with anything that is generally provided as open access, there is always the risk of deterioration due to the “tragedy of the commons.” There is a reason pure peer-to-peer platforms have not generally scaled well outside of established communities: it takes a lot of time and energy to create trust from scratch with each transaction.

As such, to be plausible for everyday use, be it in supply chain management to insurance to healthcare — where dollars effected will be much greater, and high risk speculation is not the expectation — these platforms will need to be supplemented by additional forms of trust. Where crowdsourcing won’t work, some form of third party verification service will be needed for many types of transactions (and yes, startups are already working on this!). But unlike the bottom right where the key to trust is the act of verifying individuals, in this case, it is simply about verifying what is being entered into the ledger. Think of it as a notary public for data entry.

This world will be very dynamic, but for some, maybe too much so. It might also take a lot of work to manage data across different networks. Finally, over time, there is a risk of corruption (see the child pornography-Bitcoin revelation as one example) and gaming of the networks.

Making it Real: The Shipping Industry in this Scenario

In this scenario, in the shipping industry, we might see the role of traditional brokers or freight forwarders go away, replaced by a distributed ledger and the peer-to-peer handoff between producers, transportation providers, warehouse owners and end recipients (inclduing consumers). Automated software would help these actors figure out the best routes and negotiate pricing directly, without someone else taking a cut or putting their priorities ahead. Logistics management would still be a requirement, but the provider of software — that would also need access all the relevant information about who, what and where — would not be dictating terms and prices or determining who can or can not participate (the analogy is keeping Uber’s software around, but not it’s management of drivers or pricing). There would be many creative ways to add value and get paid for it.

What this Means for Strategy and Competition

Looking across the scenarios, there are a number of insights about what it will mean to compete in each of these worlds, and therefore, what companies need to be considering in their own strategies.

In the official future, Ecosystem Giants, you must either create and grow your own integrated platform, or figure out a way to play within someone else’s. The former will be hard for most consumer facing companies, as the leading platforms already own the biggest advantages in the number of participants on the platform, and the amount of data and consumer loyalty they possess. Instead, having a high degree of differentiation will be required to avoid paying a large toll to the ecosystem leader — or potentially going out of business.

In the upper left, you are most likely going to play the role of a utility — emphasizing reliability and operating excellence — or else become a provider of expensive, luxury experiences.

In the upper right, there may be many different roles to play. Having a more distributed platform means its harder for anyone to be a gatekeeper. But at the same time, this limits the ability to grow large and it will be hard to maintain a stable position in the market without constant reinvention. And as another option, some companies will focus on support services, such as data acquisition and verification.

Finally, in the bottom right, there will be some companies that vie to be the core data provider — and room for a few different types — while others fight for attention building the coolest experiences — be it goods or services — along with the best algorithms.

Depending on the scenario that actually emerges, your strategy may need to look a lot different than it does today. In some cases, this will be a relatively easy shift. In others, it will require much greater transformation, including rethinking organizational design, partnerships and talent needs.

Notes On These Scenarios

First, these scenarios are meant to start a conversation, not end it. As is the practice in scenario planning, I am eager to update and improve the model based on the even deeper knowledge that many of you reading this are likely to have. Feedback — and corrections — are welcome!

Second, scenarios are simply scaffolding and rough drafts for what a future might look like. What I have presented here are archetypes meant to simplify the message. How things play out in actuality could look a little different from all of these — and may in fact, contain pieces of all of them. It’s especially true that we might see the future of platforms play out a differently in different regions of the world given variances in cultural and political dynamics.

Finally, keep in mind that scenarios are hypotheses about the future. They are not predictions, since no one has definitive data about the future. That said, as policy makers or market leaders, they can be used to imagine the type of future that is preferred and identify the levers that may be available to steer the future in that direction. As market players, who may have less control, they can be used as a way to map out the various options for competing that your company may need to have ready pending which scenario emerges and when. Please use them wisely.

Matt Ranen is a scenario planning and strategy consultant, helping organizations navigate future change and uncertainty. More about futures and scenario planning may be found at www.ranenconsulting.com, or follow Matt on Twitter (@MattRanen).